.png)

The Cut Through Quarterly – Q2 2025 delivers a rigorous analysis of Australian startup investment activity during the second quarter of the year. Despite a pullback in total funding from Q1’s highs, the report captures continued investor enthusiasm for early-stage deals, emerging sector trends, and signals of a maturing venture ecosystem.

This report combines detailed funding data from 76 deals with survey insights from 115 investors, offering a timely, factual snapshot of the market's current dynamics and future outlook.

Market Overview and Funding Volume

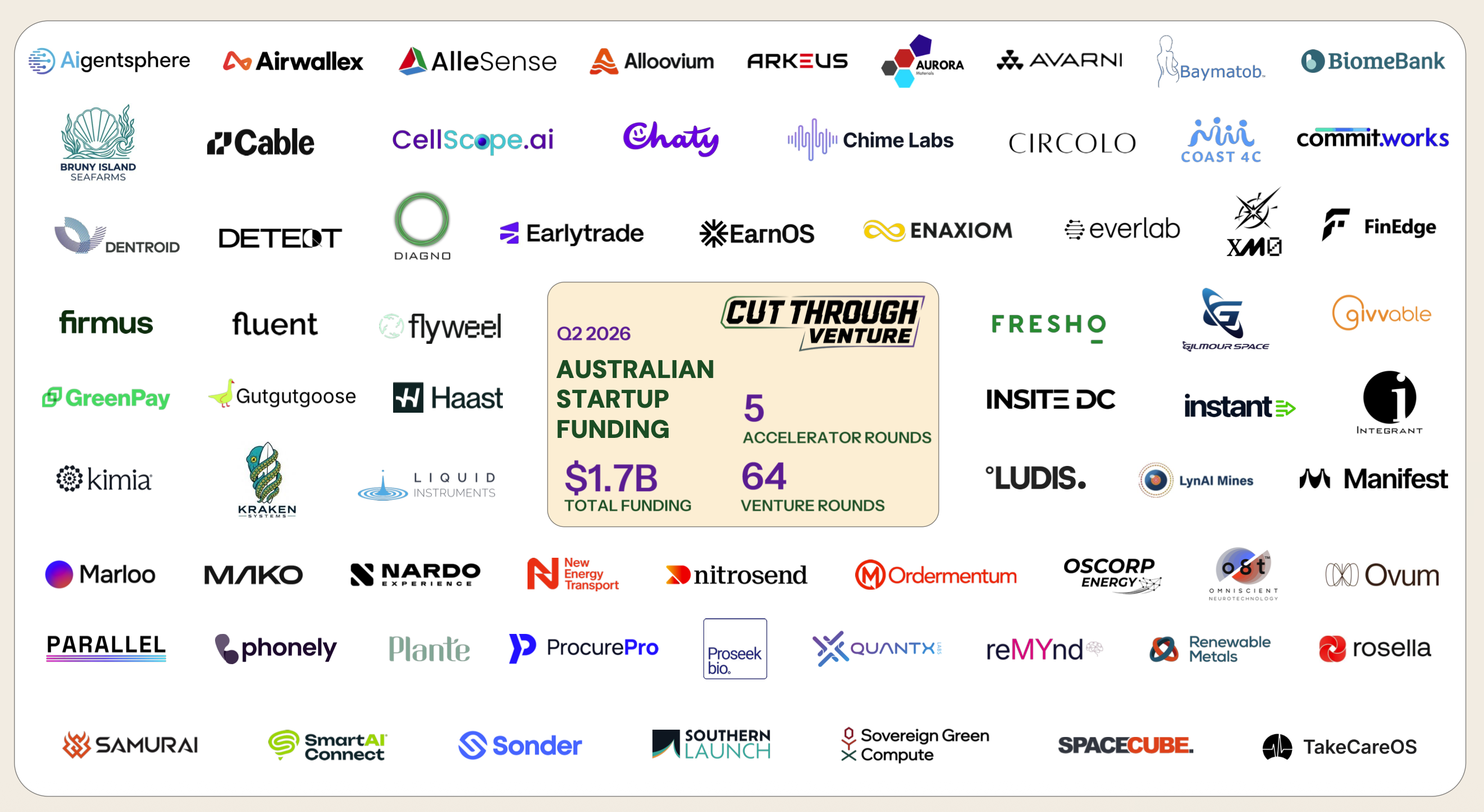

$812 million raised across 76 announced rounds, a sharp decline from Q1’s rebound.

Deal count hit a two-year low, with only two deals above $50M.

Just $4.5 million was enough to make the top 30 raises, underscoring the absence of mega-deals.

The drop ended three consecutive quarters of incremental growth in dollars deployed.

Top Sectors by Capital Raised

Fintech reclaimed the top funding spot—driven largely by Airwallex’s $232M raise.

Climate Tech and Biotech maintained top-five funding status for the fifth and eighth consecutive quarters, respectively.

Artificial Intelligence entered the top five funded sectors for the first time and now dominates deal flow.

Sectors by Deal Count

AI, HealthTech, and Climate Tech led deal volume.

More than 50% of software companies now pitch an AI-enabled product—AI has become table stakes rather than a differentiator.

Early-Stage Momentum and Valuations

Early-stage deals remained the focal point for investors, particularly pre-seed and seed rounds.

Sub-$5M rounds fell to an 18-month low, but select pre-seed deals closed in under two weeks.

Median deal sizes dipped slightly at pre-seed, seed, and Series A levels from Q1 highs.

Valuation expectations remain steady: 75% of investors expect no changes through the rest of 2025.

Sentiment Indicators

90% of investors rated Q2 deal flow as "good" or "excellent."

55% plan to do more deals than in 2024, the highest level in several quarters.

Fundraising from LPs fell to the lowest priority for VC firms, indicating confidence in existing capital reserves.

Portfolio Trends

30% of investors reported at least one portfolio company shut down in Q2—double the rate of Q1.

Layoffs eased but venture debt usage declined, a sign of stabilising balance sheets.

Gender Representation Remains a Weak Spot

Female-only teams received less than 0.5% of total funding—on track for the lowest year on record.

Only 11 deals involved a female founder.

Nearly 90% of capital to mixed-gender teams went to a single company: Airwallex.

Macro Forces Shaping the Ecosystem

Investors are increasingly focused on capital efficiency, execution readiness, and operational discipline.

New superannuation tax reforms may discourage high-net-worth individuals from investing via SMSFs, posing risks to capital inflows.

Startups are shifting from “growth at all costs” to “scalable systems before seats”, with flexible hiring, automation, and lean expansion as core strategies.

Conclusion: Early-Stage Appetite Endures Amid Cautious Optimism

Q2 2025 highlights a market recalibrating after early-year optimism. While deal volume contracted, investor appetite remains strong—especially for early-stage startups with clear operational rigor and compelling sector alignment in AI, climate, and health. With macro pressures rising, founders are advised to raise deliberately, operate lean, and act fast to secure follow-on rounds.

Access the Full Report

Get in-depth insights into funding trends, investor sentiment, sector momentum, and startup strategies in Cut Through Quarterly – Q2 2025. Ideal for founders, VCs, analysts, and ecosystem builders.