.png)

Cut Through Quarterly Q1 2023: Navigating the Slowdown

Dive into the comprehensive analysis of the Australian startup funding landscape in Q1 2023. Discover key investment trends, shifting investor sentiment, sector performance, and the state of female founder funding in Cut Through Venture's latest quarterly report.

The first quarter of 2023 marked a significant shift in the Australian venture capital landscape. After years of robust growth, the startup funding ecosystem experienced its most challenging start since 2019. Cut Through Venture's inaugural Quarterly Report provides an in-depth analysis of thisevolving environment, moving beyond monthly digests to offer deeper insightsdrawn from funding data and exclusive investor sentiment surveys. Understand the forces shaping Australian startup investment and gain critical intelligence to navigate the months ahead.

A Cautious Start: Q1 2023 Funding Declines Significantly

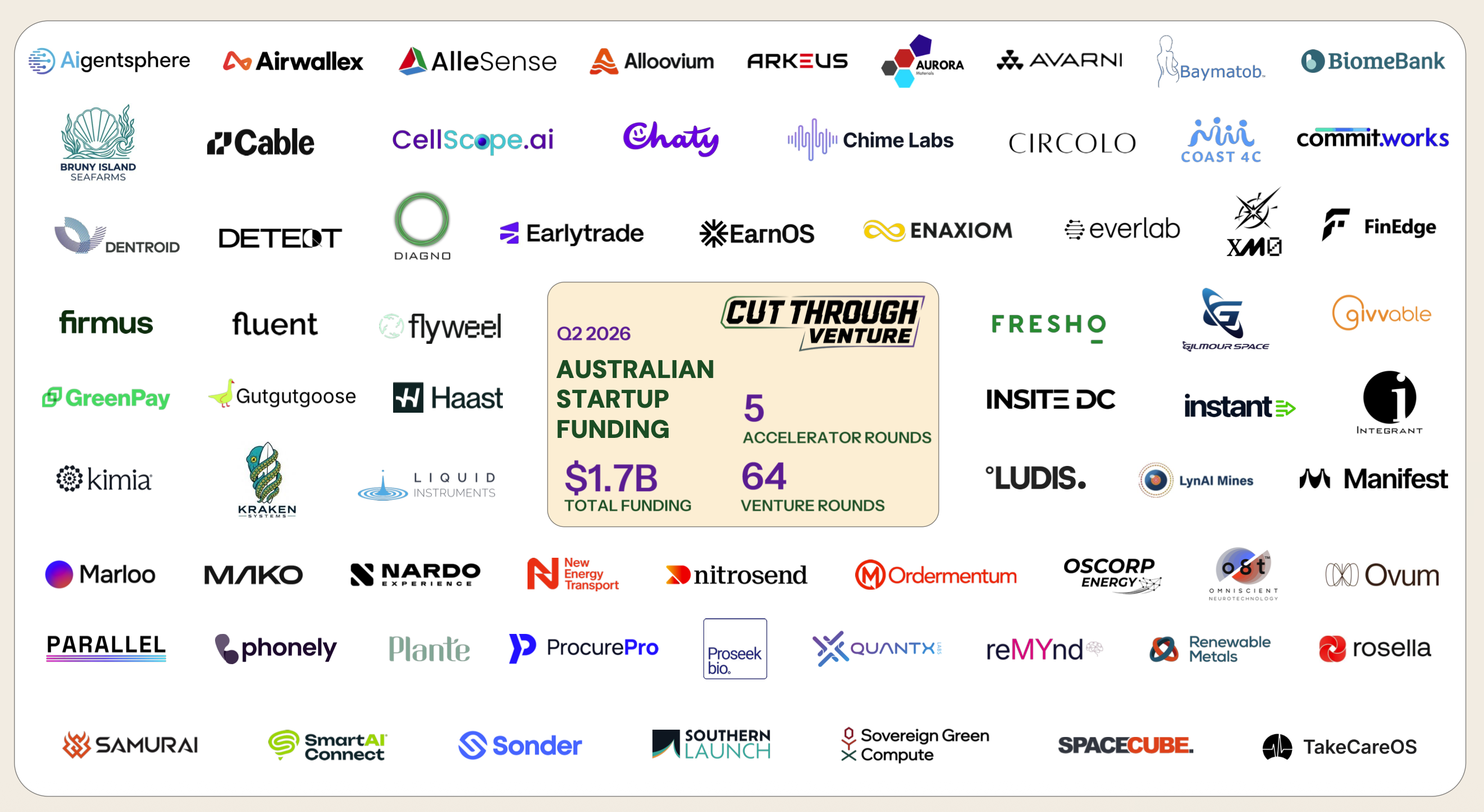

Australian startups announced a total of $661 million raised across 82 deals in Q1 2023. This figure represents a stark contrast to previous years, amounting to less than half the funding recorded in Q1 2021 and merely a fifth of the capital raised in Q1 2022. The slowdown was felt across the board:

Overall Funding: The total capital raised dipped below levels seen even in early 2020.

Deal Volume: Announced deals up to $50M reached lows not seen since Q3 2020. The most significant drop occurred in deals between $5M and $20M.

Mega Deals: Large deals ($50M+) came to a near halt, with only two exceeding this threshold, a significant drop from the quarterly average seen in 2022. Overseas investor participation in large rounds was notably reduced.

Investor Sentiment Shifts Amid Economic Headwinds

Our Q1 2023 survey, capturing insights from 141 Australian startup investors, reveals a cautiousoutlook:

Market Perception: Only 26% of surveyed investors described the Q1 funding market as favourable.

Valuation Expectations: A striking 85% of investors anticipate startup valuations will continue to fall throughout the year. Significant drops were reported compared to the previous year, with medianfalls of 30% for Pre-Seed/Seed, 40% for Series A+B, and 50% for Series C+ deals.

Funding Strategies: Reflecting the challenging conditions, over half (57%) of investors advised their portfolio companies to prioritise internal bridge rounds over seeking new external funding.

Future Outlook: Despite assessing fewer deals in Q1,79% of investors expect to complete the same number or more deals in 2023 compared to last year, perhaps indicating anticipated opportunities later inthe year.

Sector Focus: Fintech Leads, AI Gains Momentum

While fundingdynamics shifted, certain sectors demonstrated resilience and captured investorinterest:

Fintech Dominance: Fintech reaffirmed its leading position, accounting for nearly one-third of total funding and 10% of alldeals. Notable Fintech deals included Till Payments ($70M), Hnry ($35M), DataMesh ($30M), and Shift ($27M).

Investor Excitement: Investors ranked AI/Big Data as themost exciting sector, followed by Enterprise Software and Cyber/Privacy. Thisreflects a global trend and a focus on technologies driving efficiency andaddressing critical business needs.

Other Key Sectors: HealthTech showed strength in dealcount, while Agriculture/AgTech maintained funding popularity. Loam Bio, anAgTech startup, secured the quarter's largest deal at $105M. Conversely,Crypto/Web3 ranked lowest in investor excitement.

Female Founder Funding: A Mixed Picture in Q1

Funding for female-founded startups presented contrasting trends in Q12023:

Funding Share Peak: Teams with at least one femalefounder secured 31% of total funding, the highest share since Q2 2020. This wassignificantly boosted by Loam Bio's large round. Hnry ($35M) and Rumin8 ($17M) were other top female-led raises.

Deal Participation: Female founders saw increased deal participation at the Seed and Series B+ stages, reaching record or near-record highs. However, Series A participation fell to a five-year low.

Valuation Gap: A significant disparity remains, withthe median deal size for female-founded startups ($2.3M) being 48% lower thanfor all-male founding teams ($3.8M) in Q1 2023.

Unlock the Full Picture: Download the Complete Q1 2023 Report

This summary provides a high-level overview of a complex quarter. For a comprehensive understanding of the Australian venture capital market, download the full Cut Through Quarterly Q1 2023 report. Inside, you'll find:

Detailed breakdowns of funding by stage (Angel/Pre-Seed, Seed, Series A, Series B+).

Month-by-month funding trends throughout the quarter.

Further analysis of investor sentiment survey data.

Complete list of the 30 largest deals.

Deeper dives into sector performance and shifts.

Extended analysis of female founder funding metrics across stages.

Insights into the methodology and data sources.

Stay informed and position yourself strategically in the evolving Australian startup ecosystem. Access the definitive data and analysis from Cut Through Venture.