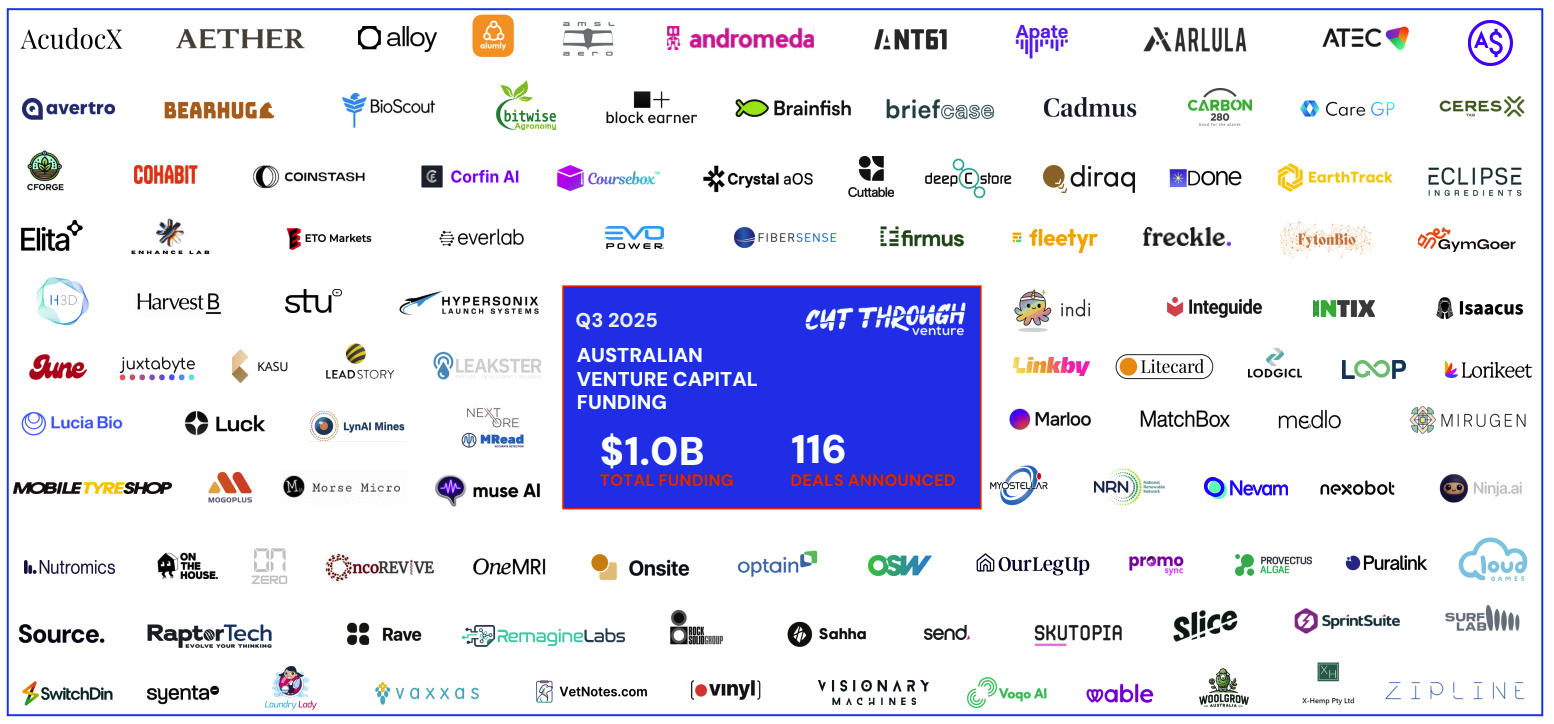

The Q3 2025 edition of Cut Through Quarterly presents an evidence-based assessment of venture activity across Australia. This quarter recorded about $1.0 billion in announced funding across 116 rounds (comprised of 85 venture rounds and 31 accelerator rounds). Results point to broad-based activity led by deep-tech categories, rising early-stage valuations, and a continued scarcity of mega-rounds. The report also tracks investor sentiment, graduation dynamics, and gender equity across stages.

Quarter at a Glance

$1.0B total funding from 116 announced rounds; biggest quarter of 2025 by deal count, lifted by accelerators.

One $100M+ round (Firmus Technologies, $330M) accounted for a large share of capital; only 17 deals cleared $10M.

Non-software sectors led funding, with hardware/robotics/IoT and biotech/medtech prominent; climate tech remained resilient.

Valuations rose at every stage, most notably at Pre-Seed, Seed, and Series A; AI-first startups priced at a premium.

Female-founder outcomes improved off a low base: female-only teams rebounded to their best result since early 2023, yet female-led and mixed teams combined were ~11% of capital, a six-quarter low.

Capital Raised & Deal Count

Total capital: ≈ $1.0B

Rounds: 116 (85 venture; 31 accelerator)

Mega-rounds: 1 ($330M Firmus Technologies)

$20–50M bracket: broadly in line with recent quarters

$10M+ rounds: 17 announced

Interpretation: Activity broadened rather than concentrated. The market remains thin in late-stage supply, while accelerators and smaller cheques underpin deal volume.

Stage Dynamics & Valuations

Median deal sizes remained at or near record highs across stages.

Dispersion widened, indicating a more polarised market—some companies command substantial rounds while others struggle to clear targets.

Valuation sentiment

Valuations moved higher at Pre-Seed, Seed, Series A; later stages steadier.

AI-first companies are raising faster and at higher valuations, reflecting strong investor demand.

Sector Activity

Hardware/Robotics/IoT topped both funding and deal counts for the first time this cycle.

Biotech/Medtech sustained strong inflows; Climate Tech extended its multi-quarter streak.

AI remained pervasive across categories (software, hardware, health, logistics), serving as an enabling layer rather than a stand-alone vertical.

Takeaway: Capital is increasingly favouring unique IP, credible regulatory/manufacturing pathways, and commercialisation in science-heavy businesses, while software categories continue to integrate AI as standard.

Largest Announced Rounds

Firmus Technologies – $330M (Hardware/Robotics/IoT)

Morse Micro – $88M (Hardware/Robotics/IoT)

Lorikeet – $54M (AI/Big Data)

Vaxxas – $49M (Biotech/MedTech)

[Logistics/Transport company] – $38M (Transport/Logistics/Supply)

(The report includes additional Series A–B+ rounds across climate, deep-tech, adtech, agtech, and more.)

Investor Sentiment & Portfolio Health

Roughly half of investors described conditions as favourable; a small uplift in “highly favourable” views.

>50% expect to complete more deals than 2024 by year-end.

Marketing/BD gained importance; fundraising from LPs remains a lower priority.

Portfolio signals

Portfolio health modestly improved; bridge rounds remain common to extend runway.

Layoffs and shutdowns stabilised; venture debt usage subdued, suggesting emphasis on discipline and efficiency.

Graduation Dynamics & Market Structure

Startups priced in the 2021–early 2022 boom still face Series B bottlenecks as growth/valuation promises reset.2024 cohort shows stronger early signals (cleaner metrics, more realistic pricing), though AI-driven exuberance requires ongoing discipline to avoid repeating past cycles.

Funding to Female Founders

Female-only teams: best quarter since early 2023, but from a low base.

Combined share (female-only + mixed): ~11% of total capital, the weakest in six quarters.

Pre-Seed representation fell to multi-year lows; accelerators accounted for much of the representation uplift.

Late stage: only one round involved a woman founder.

Implication: Structural gaps persist beyond accelerators—especially at Pre-Seed and post-Series A—highlighting the need for targeted pipeline and follow-on support.

What to Watch in Q4

Set-up is constructive if current conditions persist; to enter the “top-3 deployment years,” Q4 would need to surpass ~$1.3B.

Late-stage supply remains the swing factor; another mega-round would materially shape the annual tally.

Valuation discipline at AI-first companies and capital flows to deep-tech will define risk-reward through year-end.

Conclusion

Q3 2025 marked the broad est deal pace of the year, anchored by accelerators and deep-tech leadership in capital raised. Valuations are trending up at earlier stages, and AI is now embedded across categories. Yet mega-round scarcity, Series B bottlenecks, and uneven gender outcomes remain central to the market’s health.

Access the Full Report

Download the full Cut Through Quarterly – Q3 2025 report to explore sector tables, round comps, and investor sentiment charts in detail.