Morning,

We gave ourselves a spring refresh: new charts, a tweaked format, and we splurged on a perky sunflower yellow.

Shout out with feedback -- good or bad.

We also took stock of all the stuff we do (or could do). We're sunsetting Startup Spotlight, so our regular emails will return to a monthly cadence. For a more regular startup newsletter fix, we recommend our friends at Overnight Success, LOI's new tech daily update, or Ignition Lane's Wrap. For those sick for health, check out What the Health.

State of Australian Startup Funding will also return in early 2023 to recap the rollercoaster ride that is 2022. Founders can also search for investors who are still funding new opportunities at our We Have Dry Powder directory.

Finally, our angel network Cut Through Angels launches very soon. We'll enable experienced and budding angels to invest alongside the best in the biz, with a minimum cheque as low as $2000. Join the network waitlist here.

Chris also recently joined Five V. If you're raising your Series A or B, email him at cgillings@fivevcapital.com.

Alrighty, let's dig in.

Build a bridge, and they will fund.

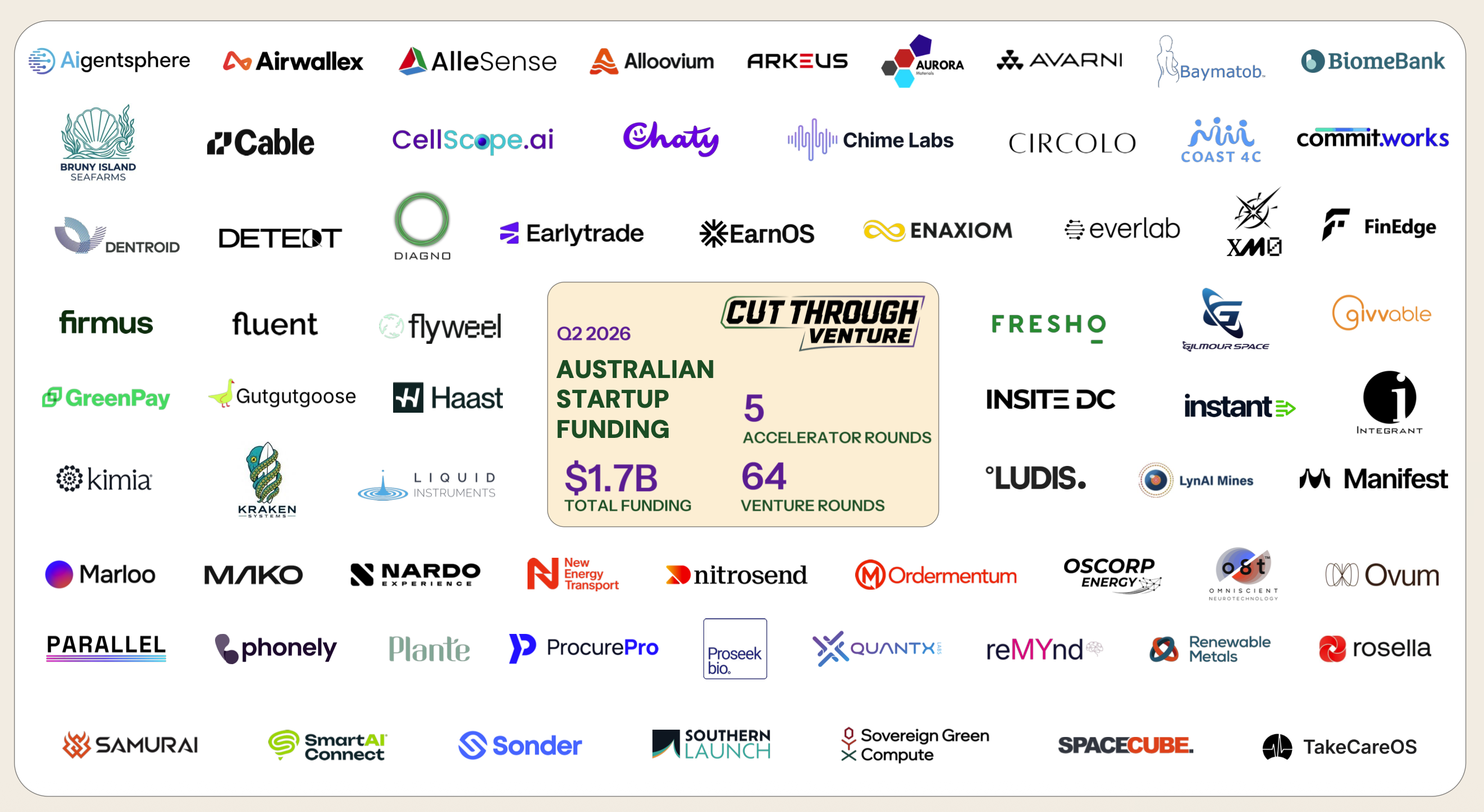

The cold funding month hot streak continued into August, with just $225M across 32 deals announced. Startup investors tend to flock to the Mediterranean for the northern hemisphere summer, so August is always a slow month for funding news. This August was especially quiet, however: half the dollars and deals announced in August 2021.

Has funding slowed? Yes. But, there is some nuance to it— a little nuance called... the bridge round.

In venture land, a bridge round is a round of financing that tides a startup over until its next larger round of funding... and they're the hottest thing to hit startup funding since the Patagonia reversible vest.

The number of bridge rounds is soaring, but their details may never be revealed publicly. Why? Because they're mostly small, at flat or lower valuations than the startup's previous round, and often funded by prior investors.

Put simply, not very sexy to talk about.

Big global funds still hunting.

AdvanCell raised to continue its work fighting melanoma, and prostate, pancreatic and breast cancer. We won't do their important work justice -- so, have a read about it here.

Top global funds continue to deploy capital into Aussie startups. Insight, which invested in device security software startup Devicie, has made three investments into local startups this year. Local cyber security services provider CyberCX joined them on the Devicie deal.

Meanwhile, Bessemer Partners clocked their first Australian investment since their bet on up-and-comer Canva, investing in global supply chain tracking startup Lumachain. Local fund Main Sequence joined them on the round.

Hysata's round will power its team's work on a new type of hydrogen electrolyser. Electrolysers use electricity to split water into hydrogen and oxygen and are the key technology for producing green hydrogen. Unfortunately, electrolysers are notoriously uneconomical -- but Hysata is on the way to flipping that.

All G Foods raised a round to continue to make us feel good on the inside with their #plantpower fueled foods. And Frank Body took a caffeinated funding hit to expand their coffee skin scrub and skincare range.

3 other deal level items to note.

Health > Wealth. Carina Biotech raised to fight cancer. They're developing a t-cell therapy that engineers a patient's immune system to target and destroy their own cancer cells, and enables doctors to use the therapy to treat a broad range of cancers. InstantScripts raised a growth round to scale its online prescription renewal platform, while Midnight Health and Splose raised to help medical practices digitise to deliver a better overall patient experience.

The anti-bad-for-you crew. Hello Clever raised a punchy Seed round to build out its anti-BNPL solution, which helps young folk manage their finances, save, and reward them for responsible spending. Immediate added to its funding stockpile to roll out its online mediation solution globally to keep squabbling ex-partners and neighbours out of the same room. ExtrasJars raised a Seed to build a set of inclusive and flexible health insurance offerings. Meanwhile, BaseUp wants to make the oh-so-luxe perk of driving to work possible for more workers across Australia and the US, and they raised to make it happen.

The crowd loves deleting draughts, and eating ugly food. Crowdfunding platform Birchal punched above its weight in August, contributing five deals to the tally. Three of those were craft brewers (Dainton, 3 Ravens, and Future Magic) -- which begs the question as to whether crowd investors are investing with their heads or their tummies. The other two startups, Farmers Pick and Good & Fugly, aim to reduce food wastage by putting less-perfect looking fruit and veg onto plates, not landfill. Time will tell whether these businesses will generate the venture-style returns crowd investors are hoping for.

Join us at the Sustainability Summit on September 16 to discover how cloud technology can help your business achieve more sustainable outcomes faster.

Register for the event and be sure not to miss a special Startups focused session Start at Zero for startups presented by Natalie Piucco | 2:15 PM AEST.

Register HereSmall numbers skew big.

Food and Beverage accounted for 32% of the deals announced, though the sector had the smallest average deal size. As mentioned above, two-thirds were crowdfunded deals.

Fintech also had a relatively busy month, with four Seeds and a Series A announced. Invoice factoring business Timelio raised an unnamed round, which was paired with the founders of the seven-year-old business calling time in their roles at the business.

The eastern seaboard states accounted for all but two of the announced deals. NSW dominated the leaderboard, taking four of the top five largest deals.

At the risk of sounding nerdy.

Median deal sizes at the Angel/Pre-Seed and Crowdfunding stages remain in line with those seen in 2021 and early 2022. In contrast, Seed and Series-B-and-later deals tumbled significantly.

The median Series A deal size appears to have increased, but that should be taken with a grain of salt. Smaller Series A deals (those bridges we spoke of earlier) are getting done, but founders and investors are staying zip-lipped about them.

At the risk of sounding nerdy, the interesting dynamic in the below chart is the compression in the median-to-average spread. Averages are influenced by outlier deals, while medians are not, and so, the data shows that far fewer outlier-sized deals are happening across all stages.

Whether we're talking sort-of, pretty, or extremely large deals, the trend is only going in one direction.

$50M+ mega deals peaked a year ago. Someday old VCs will tell young VCs about those good old days: when the likes of Canva, Airwallex, Go1, Scalapay, Employment Hero and CultureAmp all raised $100M+ rounds in a matter of months, and almost every round over $50M had a big brand global investor in the mix.

Problem solved 😉.

Funding to 100% female founding teams continues to trend above the long-term average, while the stats teams with at least a mix of genders remain tightly bound to long-term levels.

The less good reality is apparent when the data is parsed out by funding stage. As rounds progress, the share of participation from non-all-male deals slips, in perfect lockstep.

And on that positive note, we'll wrap.

Thanks for sticking to the end. See you next month.

– Chris + Sharon.