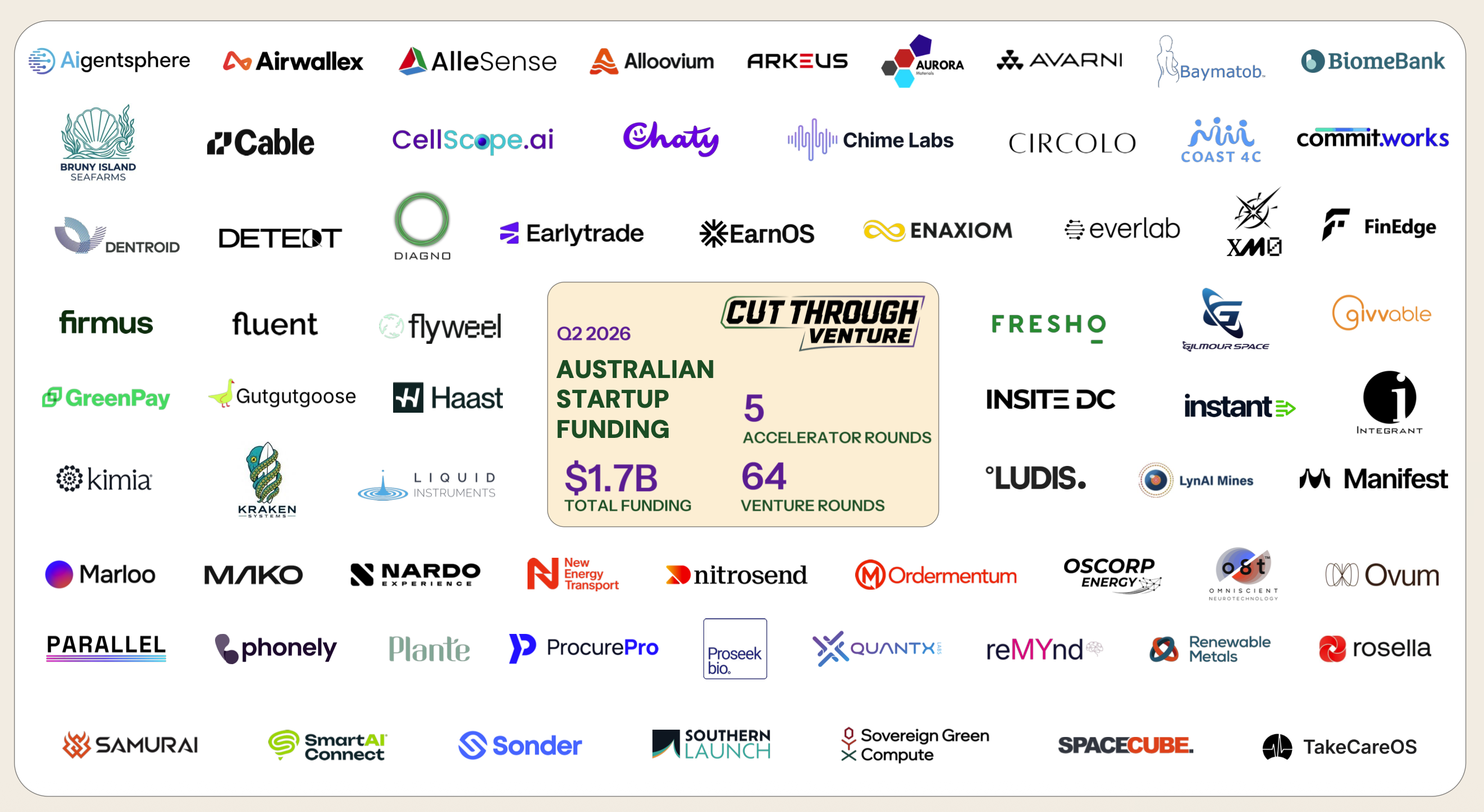

The "State of Australian Startup Funding 2024" presents a data-rich analysis of the evolving venture capital landscape in Australia. Following a turbulent 2023, this year’s report identifies green shoots of recovery across early-stage funding, gender equity, sector-specific momentum, and international investor interest. Based on 414 deals totaling $4.0 billion, the third-highest annual total on record, the report captures investor sentiment, founder behavior, and macro trends shaping Australia's innovation economy.

The Australian Funding Landscape in 2024

Overall Market Conditions

Total capital raised: $4.0B across 414 deals, up 11% from 2023.

Highest funding months occurred in the second half of the year.

AI and sector-specific resilience buoyed confidence despite low M&A and IPO activity.

Deal Size and Round Trends

Pre-Seed median deal size: $1M (record high).

Seed median deal size: $3M (record high).

Series A and B+ rounds: smaller but more strategic.

22 deals exceeded $50M, up from 15 in 2023.

Sectoral Leaders and Shifts

Top Funded Sectors

Fintech: $947M (up sharply from 2023).

Climate Tech/CleanTech: $609M across 55 deals (most by volume).

Biotech & MedTech: $347M.

Sector Trends

AI’s influence visible in enterprise SaaS, Fintech, and HealthTech.

Climate Tech faces funding gap at scale-up stages despite deal count strength.

Strong investor interest in Space/Aviation/Defence, Cybersecurity, and Deep Tech.

Founder & Investor Dynamics

Gender Equity and Team Composition

Women-founded teams participated in:

42% of Angel + Pre-Seed deals (vs 27% in 2023).

29% of Seed rounds (vs 20% in 2023).

19% of Series A; 16% at Series B+.

Share of capital raised by female founders fell to 15%, down from 18% in 2023.

International Capital and LP Sentiment

57% of deals included international investors.

63% of startups sought overseas funding to scale.

LP sentiment remains cautious: 23% of firms closed a fund in 2024, but 37% raised less than targeted.

Investor Sentiment and Outlook

Valuation Stability and Deal Structuring

Valuations began to stabilize after 2022–23 declines:

Pre-Seed/Seed: ~11–12% up from 2023.

Series A/B: ~7% up.

However, effective valuations often lag due to liquidation preferences and structured terms.

2025 Outlook

74% of investors expect higher deal volumes in 2025.

Growth anticipated in AI, HealthTech, and ClimateTech.

Macro conditions, M&A/IPOs, and institutional LP activity will shape trajectory.

2024 signals a maturing and resilient startup ecosystem in Australia. With record early-stage deal sizes, strong sector-specific activity, and a deliberate investor focus on fundamentals, the Australian venture market is poised for sustained growth. However, success hinges on tackling scale-up funding gaps, advancing gender equity, and ensuring LP engagement.

Explore the full report to gain:

State-by-state funding breakdowns and sector-level investment patterns

Expert commentary from leading investors and fund managers

Benchmark data for founders and startup operators